Three Trillion-Dollar IPOs. One Pool of Capital.

The capital pool math is well known. What it explains about pricing, lawsuits, and subsidies is not.

The capital pool math has been making the rounds. Fortune called it a potential drain. Tomasz Tunguz ran the float analysis in February and called it ‘a boulder in a pond’. They are both right. But the conversation has mostly stayed at the level of the arithmetic: big numbers, finite pool, somebody gets squeezed. What no one seems to be connecting is that the capital squeeze explains the recent behaviour. Every pricing decision, product launch, and every lawsuit timing in the AI industry right now makes more sense when you read it as an IPO positioning play rather than a technology decision.

Start with the arithmetic, because it’s the table stakes:

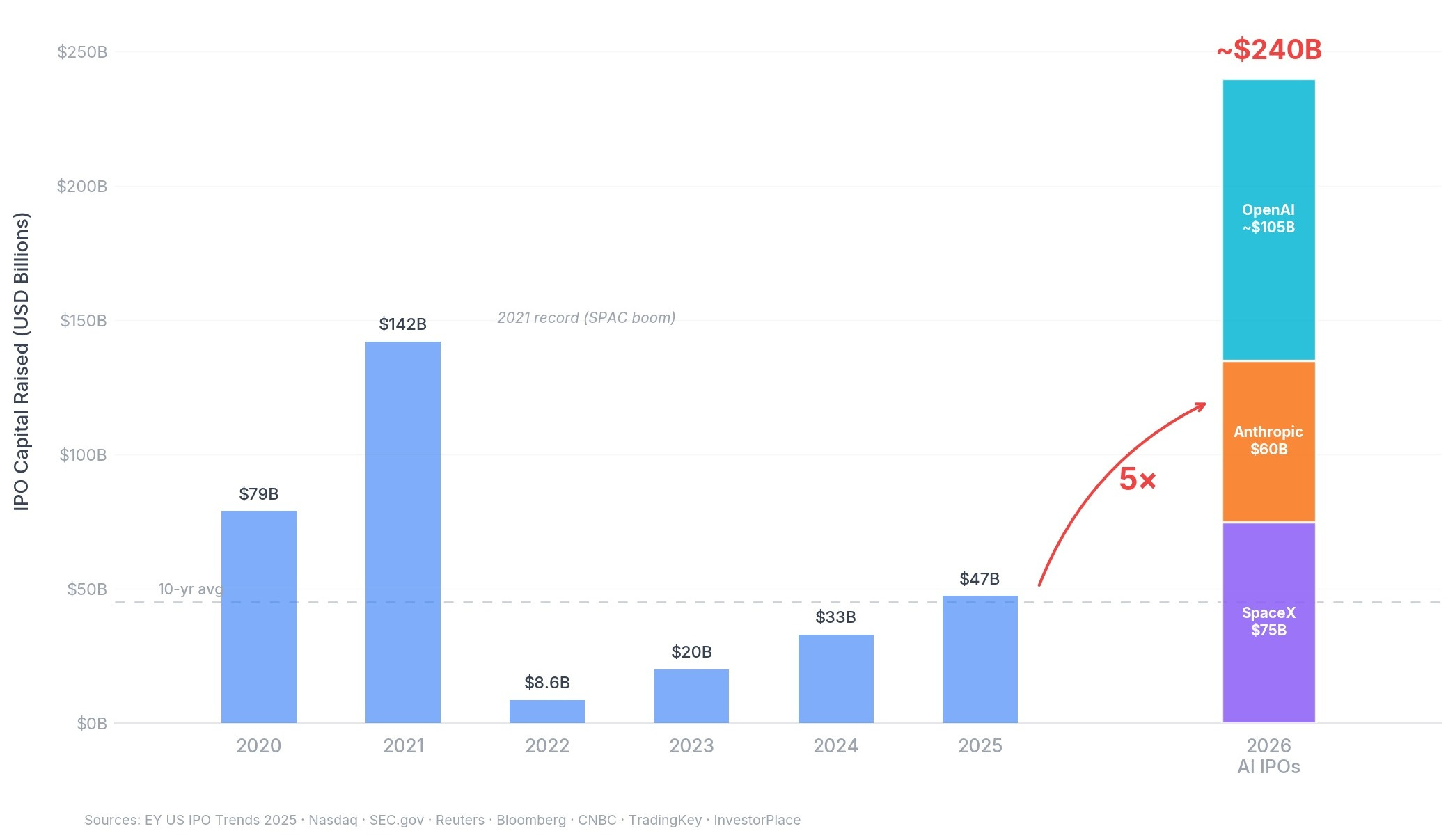

SpaceX, now merged with xAI, wants to raise approximately $75 billion in its IPO at a valuation of up to $1.75 trillion. The roadshow is planned for the week of June 8.

OpenAI is targeting Q4 2026 at a valuation approaching $1 trillion, having just closed a $122 billion private round at $852 billion.

Anthropic is planning an October listing, aiming to raise over $60 billion at a $380 billion valuation.

Add it up. It’s an enormous amount of cash.Three companies are trying to extract somewhere between $200 and $240 billion from public markets in a single quarter.

This number is nearly 5X larger than the $47.4 billion that the entire US IPO market raised in 2025. 2025 was a big year too. The 10-year pre-pandemic average was $45 billion annually. Cumulative capital raised through all US IPOs from 2016 to 2025 was roughly $469 billion. Three companies want half of that in one quarter.

That’s the arithmetic. It’s correct and it’s important. But it’s not the story. The story is what companies do when they know the pool is finite.

Once you accept the pool is finite, every move these companies have made in the past six months reads differently.

Musk merged xAI into SpaceX in February, creating a combined entity that bundles orbital launch, satellite broadband, a social media platform, and a frontier AI lab into a single offering. The IPO paperwork could be filed this month. That’s not engineering urgency. That’s capital urgency. He wants to be first in the pool because the first swimmer gets the most water.

Meanwhile, Musk’s lawsuit against OpenAI went to trial on April 27 in Oakland. He’s seeking $130 to $150 billion in damages, alleging Altman abandoned OpenAI’s founding nonprofit mission for personal profit. The trial is expected to run through mid-May. OpenAI itself listed the litigation as a risk factor in documents distributed to investors during its latest fundraise. Whether or not the suit is designed as a strategic delay, it functions as one: an active federal trial during the months when OpenAI needs to be building investor confidence for a Q4 listing. OpenAI characterises the lawsuit as part of a broader pressure strategy in favour of xAI. Draw your own conclusion. A lawsuit that depresses OpenAI’s IPO reception by even 10% redirects billions of dollars toward the remaining listings.

First is best in a finite pool. Every week one company’s IPO is delayed is a week another company’s roadshow gets a clearer run.

3+1 (+1) Titans

The revenue pressure tells the same story from a different angle. OpenAI’s annualised revenue hit $25 billion in early 2026, up from $13 billion in 2025. Impressive growth, but the company missed its internal target of 1 billion weekly active users, landing at around 900 million. It missed multiple monthly revenue targets in early 2026. The CFO, Sarah Friar, has publicly expressed reservations about the listing timeline and spending plans. Morningstar published an analysis in late April arguing that mid-to-late 2027 is the more realistic window.

And here’s a detail that should be getting more attention than it is. Bloomberg reported that after contacting hundreds of institutions, one secondary market firm found “not a single one willing to buy OpenAI.” These aren’t retail investors. These are the institutions that receive 80-90% of IPO share allocations. If the buyers who matter most for a successful offering are already passing in private markets, the Q4 listing has a structural demand problem that no roadshow fixes. Musk said he wasn’t surprised. Anthropic’s share of combined enterprise spending with OpenAI went from 10% in early 2025 to over 65% by February 2026, according to Ramp Economics Lab. The enterprise market, where durable recurring revenue lives, is moving toward Anthropic. OpenAI’s consumer moat is real. Its enterprise moat is narrowing.

The pool gets even more crowded when you add SoftBank, which is simultaneously planning to list a new robotics and AI spinout called Roze at a $100 billion valuation while also being one of OpenAI’s largest investors, having committed $30 billion across the latest funding round. Even at a modest 10% float, Roze puts another $10 billion into the same institutional capital queue, from a company financially entangled with one of the three main listings.

Pricing Behaviours

This is why the pricing behaviour of these companies in the past three months makes more sense as IPO preparation than as competitive strategy. Anthropic killed flat-fee enterprise pricing in April, moving from $200-per-seat all-you-can-eat to $20 plus per-token consumption billing (I wrote on this last week). That’s not a product decision. That’s a margin decision. The flat fee was a venture subsidy, the same playbook Uber ran for nine years: price below cost, create dependency, then reprice when the customers can’t leave. The IPO demands the repricing because public-market investors need to see a path to margin, not a path to more subsidised growth.

OpenAI is doing the same thing from the consumer side. Getting hundreds of millions of users onto paid plans creates the revenue narrative an IPO needs. But it also signals something uncomfortable: the willingness to pay for AI at the consumer level is still thin. The. latest news is a $8/month plan. This is a SAM expansion tactic. for pre-IPO momentum. The average small business doesn’t have the infrastructure to turn an AI subscription into operational leverage. They can make presentations and draft emails, but the gap between “I have access to the tool” and “the tool is embedded in how I operate” is wider than the demos suggest.

Remember Netscape? Bankers do.

There’s a historical echo here that’s worth paying attention to. Morningstar made the critical observation: whichever company lists first defines the public market multiple for frontier AI. OpenAI is at risk of entering a valuation framework it did not set, on terms it cannot control, behind competitors that got there on a fraction of the capital.

This happened before. In the browser and search eras, the first major IPO set the pricing framework for every company that followed. Netscape’s 1995 listing at a $2.9 billion market cap on zero profits established what the market was willing to pay for internet potential. Every internet IPO that followed was priced against the Netscape benchmark. When Google listed in 2004 at $23 billion, it set the template for search and advertising companies for a decade. The first mover didn’t just raise capital. It set the valuation language everyone else had to speak.

Right now, SpaceX is positioned to be Netscape: the first massive listing that tells the market what AI-adjacent companies are worth. If SpaceX lists at $1.75 trillion and the market absorbs it, the valuation framework for OpenAI and Anthropic gets validated. If SpaceX stumbles or absorbs so much capital that the market has indigestion, the companies behind it face a colder reception. The largest IPOs in a given year tend to underperform the market in their first year. The bigger the debut, the more fragile the aftermarket.

The pre-season really matters

The arithmetic is well understood. What’s under appreciated is how it connects. The capital squeeze doesn’t just determine which companies list successfully. It determines how every company in the AI industry prices its products, structures its subsidies, and treats its customers in the 12 months before the listing window opens. These are not three independent companies independently deciding to go public. These are three companies whose pre-IPO behaviour is being shaped by competition for the same finite pool of market capital.

The sophisticated counterargument is that these IPOs will create their own demand. S&P, FTSE Russell, and Nasdaq are all considering fast-track index inclusion rules that would bypass the normal 12-month seasoning period and add these companies to major indices within days of listing. Yes, you are reading that correctly. The massiveness of these three companies are rewriting the public market rules.

If successful in index fast-tracking, Bloomberg Intelligence estimates this could force $24 to $48 billion in mandatory passive buying from index funds almost immediately.

That’s real money. But it’s constrained by float. SpaceX is raising $75 billion at a $1.75 trillion valuation, putting roughly 4% of shares into public hands. You can’t pour $48 billion of index money into $75 billion of tradeable supply without massive price distortion. The passive demand is real but it doesn’t solve the $240 billion problem in a $47 billion market. And if ByteDance enters the same window, as rumoured, the capital math goes from strained to structurally impossible.

SpaceX moves first and moves fast. The Musk lawsuit keeps OpenAI’s legal risk in the headlines during its pre-IPO window, whether that’s the intent or the side effect. Anthropic sits in October, hoping to benefit from enterprise momentum and whatever valuation framework the first listings establish. And the market has to decide whether it can absorb $250 billion or more in AI-adjacent IPOs in a year when the entire IPO market has never cleared more than $142 billion. The maths doesn’t work for all of them. Somebody is going to get squeezed.

If you’re an investor, watch the sequence, not the valuations. If you’re an enterprise buyer, watch the desperation for revenue, because it explains every pricing decision, every free tier expansion, and every subsidy these companies are offering in the months before they need to show public-market investors a growth story. The IPO doesn’t just change who owns the company. It changes what the company optimises for. And when three companies are optimising for the same pool of capital at the same time, the customers are the product.

Sources

SpaceX IPO: roadshow June 8, prospectus late May, $75B raise, $1.75T valuation (Reuters, Bloomberg, CNBC, TradingKey)

OpenAI: Q4 2026 target, $852B valuation, $122B private round, $25B ARR, missed 1B WAU target, $14B projected 2026 loss (CMC Markets, TECHi, Morningstar, WSJ, Medium)

Anthropic: October 2026 target, $380B valuation, $60B+ raise (TradingKey, InvestorPlace, Yaabot)

US IPO market: $47.4B raised in 2025, $469B cumulative 2016–2025, pre-2020 10-year avg $45B/yr (EY US IPO Trends, Nasdaq, Yaabot)

Musk v. OpenAI: trial began April 27, 2026, Oakland, $130–150B damages sought, expected through mid-May (CNBC, Fox Business, Washington Post, Trending Topics)

“Not a single institution willing to buy OpenAI” on secondary market (Bloomberg via TradingKey)

Anthropic enterprise share: 10% → 65% of combined spend, early 2025 to Feb 2026 (Ramp Economics Lab via Yaabot)

Morningstar: mid-to-late 2027 more realistic for OpenAI listing (Morningstar, April 2026)

Largest US IPOs: tend to underperform in first year (Jay Ritter, University of Florida, IPO performance research)

Fast-track index inclusion rules: S&P, FTSE Russell, Nasdaq considering bypassing 12-month seasoning; $24–48B forced passive buying (Bloomberg Intelligence via InvestorPlace)

SoftBank Roze: $100B target valuation (~$10B estimated raise at 10% float), H2 2026; SoftBank invested $30B in OpenAI (FT, CNBC, TechCrunch, Benzinga, SaaStr)

SpaceX float: ~4.3% implied ($75B raise / $1.75T valuation); 30% retail allocation confirmed (CNBC, Reuters, Bloomberg)

Interesting article. What stood out to me wasn’t so much the valuations themselves, but the reality that when this level of capital, infrastructure and market attention concentrates into a very small number of AI companies, it inevitably becomes harder for everyone else operating in the space. Not necessarily because smaller companies have worse technology, but because they’re competing against subsidised growth, massive distribution, investor gravity and ecosystem scale. It probably means the next few years reward businesses that are genuinely embedded into real workflows with clear economic value, rather than those relying on momentum or broad AI narratives alone.